The release of DeepSeek R1 at the start of the year sent shockwaves through the global AI industry, proving that China could develop advanced, high-performing models at a fraction of the cost of Western competitors – despite U.S. export controls and resource constraints. This breakthrough challenged assumptions about the scalability, economics, and accessibility of state-of-the-art AI, and triggered reevaluations among investors, tech firms, and policymakers worldwide.

Given these dramatic shifts, we have been trying to better understand AI developments in China. We also wanted to understand the broader impact of these developments on other sectors and companies. So I recently joined an AI- and robotics-themed trip organised by Tech Buzz China to Shanghai and Hangzhou. On the trip, I met several Chinese AI unicorns along with other AI and robotics startups.

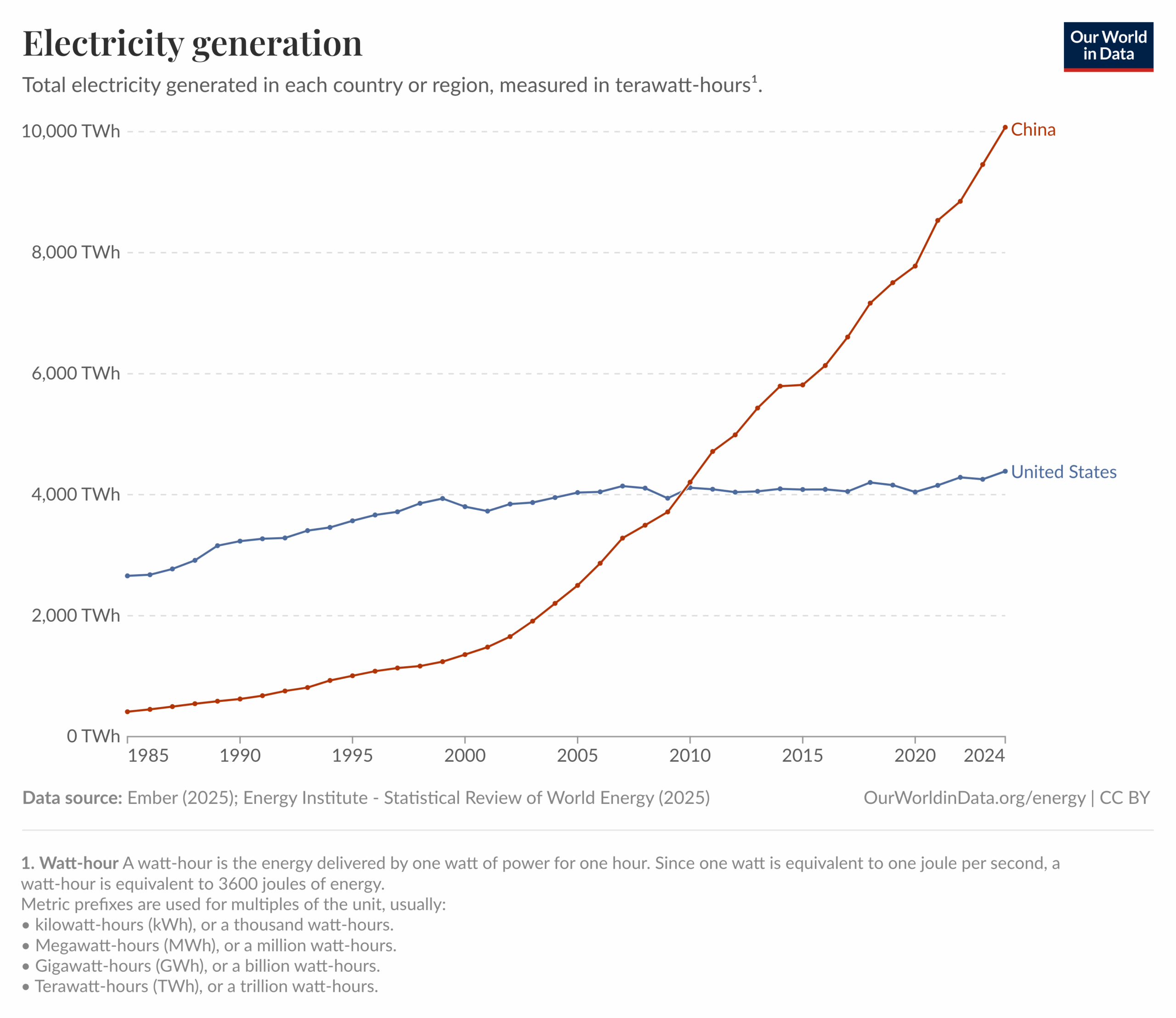

We think the Western media is underestimating the pace of AI development in China. China is catching up and pulling ahead in AI development. The Chinese government is pushing hard to streamline AI and Robotics development through significant incentives. In the US, a key bottleneck in building AI data centers is power which is not an issue in China (see following chart).

A striking trend throughout our trip was the acceleration of open-source development as a cornerstone of China’s AI strategy. Companies like DeepSeek and Alibaba are releasing powerful models under open licenses, fostering rapid innovation, lowering adoption barriers, and cultivating thriving developer communities within and beyond China’s borders. This open approach is enabling these firms to outpace traditional, closed-model peers in acceptance and ecosystem growth.

Confronting the reality of ongoing U.S. export controls on advanced chips, Chinese AI companies have responded with ingenuity. By pursuing architectural innovations and emphasizing algorithmic optimization, industry leaders minimize their need for top-tier semiconductors. Domestic efforts, such as Huawei’s development of homegrown GPUs, underscore a broader push toward technological autonomy.

At the World AI Conference (WAIC) in Shanghai, Huawei showcased its latest CloudMatrix 384 system. Industry analysts view it as a direct competitor to Nvidia’s GB200, the U.S. chipmaker’s most advanced system-level product currently available in the market. Huawei still has a long way to go to catch up with nVidia and AMD. However, by restricting sales of advanced chips to China, the U.S. government has given China a strong incentive to develop homegrown alternatives.

Where Chinese companies truly shine is in the realm of applied AI. Robotics, autonomous vehicles, and sector-specific solutions dominated our meetings, with local players successfully integrating cutting-edge AI into tangible products for manufacturing, logistics, and consumer use. The focus on delivering practical, bottom-line value to end-users marks a noteworthy contrast with Western markets where experimentation and academic benchmarks often take precedence.

Notably, the prevailing attitude among founders and executives was pragmatic. Conversations were centered not on distant existential questions or speculative risks, but on innovation that drives immediate business outcomes. Most of the founders we met saw AI as a tool with which they could solve real-world challenges for partners and customers today.

China’s close-knit manufacturing and innovation ecosystem stand as a powerful enabler of this momentum. This is particularly visible in the robotics sector. Proximity to advanced factories and supplier networks enables teams to iterate at a high speed, translating lab breakthroughs into commercial deployments in weeks rather than months. This tight integration of R&D and manufacturing is a critical competitive edge unique to the region.

One example of this was Hangzhou based Fancy Tech which aims to “make anyone’s idea become a popular sellable product globally – in just one week”! Fancy Tech is moving far beyond its original e-commerce marketing roots by embedding itself directly within the manufacturing supply chain. Leveraging its proximity to China’s dense network of factories and suppliers, the company is now integrating its AI-driven solutions with core manufacturing processes—a feat that would be difficult for non-Chinese competitors to replicate due to the unique regional infrastructure.

Lastly, the organizations we visited displayed an impressive level of operational efficiency. Many of these AI startups run exceptionally lean. They are leveraging AI not just in the products they build, but across internal functions: coding, design, marketing, and even research are often turbocharged by automation and intelligent workflows. Though impressive, this is also a worrying sign as these AI tools will lead to significant job losses in multiple industries. We are already seeing early signs of job losses in the traditional IT sector as well as large technology companies which were early to adopt AI coding tools.

Our China trip revealed an AI ecosystem that has moved beyond the “imitation” phase to become a genuine innovation center with distinct competitive advantages. The traditional binary view of U.S. technological dominance versus Chinese catch-up is inaccurate. The combination of state support, cost-efficient engineering, and rapid commercialisation capabilities positions Chinese AI companies as formidable global competitors. For us, this represents both an opportunity to invest in innovative technologies at attractive valuations and a necessity to understand the evolving competitive landscape in one of technology’s most important sectors.

As a general-purpose technology, AI will pervasively transform how businesses operate, compete, and create value across virtually every sector. To successfully navigate this trend, we must identify which established business models are vulnerable to AI-driven creative destruction and where new value creation opportunities will emerge.

In Pt 1 (here), I introduced the American networking company Ubiquiti Inc and its founder Robert Pera. I discussed Ubiquiti’s products and their aggressive share buybacks.

In Pt 2 (here), I explored Ubiquiti’s unique business strategy and the reasons behind their high profitability.

Finally, in this third part, I’m putting together some of the most common questions we have been asked regarding our investment in Ubiquiti.

1) How do you go about forecasting the company’s revenue? And if you don’t have visibility, how do you get comfortable with that?

We spent a lot of time thinking about the opportunity size and the total addressable market. However, the company operates in segments where even management themselves didn’t really understand how big the end-markets could be. Secondly, they have entered new areas with new products several times. Given their history of innovation, we have decided to be patient and let things play out. We don’t forecast but we do track their progress.

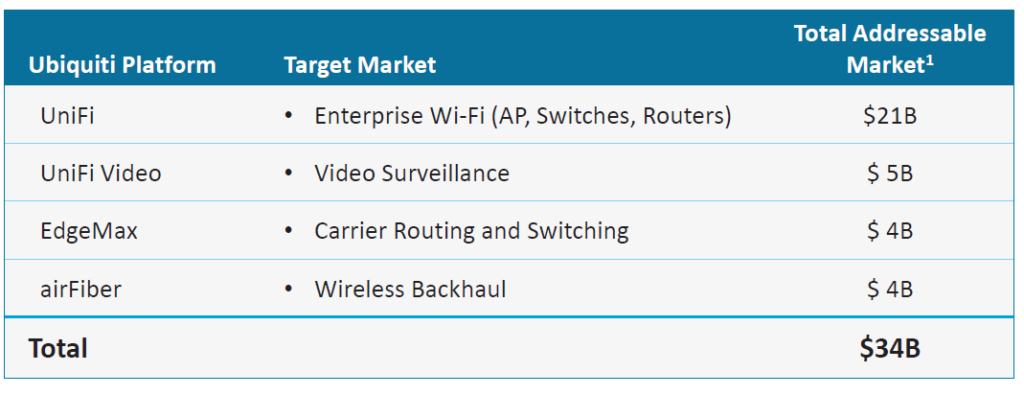

Still, it is instructive to look at the company’s own TAM estimates. The table below is from a company presentation in 2017:

2) Is this a good business?

Yes, indeed. Just look at the historical free cash flows and return on invested capital – all while maintaining good growth.

Let’s go back and revisit the chain of events from 2017.

On 3rd Aug 2017, Ubiquiti announced good results and guided strong FY18 growth: revenue and EPS were expected to grow 24% and 29% y/y respectively, based on the midpoint of the guidance range. Management was also very positive on the outlook for the company’s enterprise WiFi products as well as the company’s potential to improve margins. The next day shares rallied over 20% and reached all-time highs in subsequent weeks.

Shortly afterwards, on 18th Sep 2017, short-seller Citron Research released a negative report on Ubiquiti causing the stock to fall sharply. The report included many allegations, the most serious being that overseas cash did not exist and that key offices and key personnel were shams.

Over the next few weeks, by evaluating the company’s responses and the reactions of other investors, we came to the conclusion that the short-seller’s allegations were largely baseless. To be fair, there were a couple of minor points in the short-seller report that were correct but they were minor lapses of a frugally run company rather than fraud.

To us, the key point was incentives: as a 70% owner, it would be against the interests of founder and CEO Robert Pera to sabotage his $3bil stake (at the time) in Ubiquiti. The company had largely been self-funded and hadn’t raised significant amounts of capital from the market. If management were committing fraud, they would primarily be defrauding themselves! Also, we noted that (1) Pera did not draw a salary from the company and (2) the company had returned cash to shareholders via share buybacks. If Pera wanted to extract money from the company, there were easier and more legitimate ways to do so, such as paying himself a hefty salary or paying dividends instead of buying back shares.

In early 2018, Ubiquiti put the main accusations, about non-existent overseas cash, to rest when it announced repatriation of $677.2 million (most of their overseas cash) from its foreign subsidiaries to U.S. banks and used this cash to further fund the company’s share buybacks.

Citron’s report said “either Robert Pera is the best CEO in networking equipment, or Ubiquiti is committing FRAUD”. If we are now convinced that Ubiquiti is not a fraud, then perhaps it is time to admit that Pera is an exceptional CEO.

4. What is your view on the market share trends, stability of market structure, market growth? Does having a market view matter more in the fast-moving world of technology?

For us, it’s less a market view and more a view on Ubiquiti’s track record of introducing innovative new products.

We don’t have a strong view on market growth though we’ve looked at projections. We do think that the Covid crisis has raised the importance of good internet connectivity. After the short term slowdown, we expect continued growth in the enterprise market.

Based on IHS Markit data, the enterprise WLAN market revenues grew at a 12.4% CAGR from CY10-18 from $2.5B to $6.4B and is expected to grow at a 7.6% CAGR CY18-23 from $6.4B to $9.2B, respectively. Now it’s worth noting that this projection is just for access points and controllers. Ubiquiti has other products in enterprise and is also targeting new product lines like cameras and door access products that they can upsell to their existing customers.

Market share data in WLAN by Revenue:

5. Is the business cyclical? Do customers treat the purchase as a major capex item?

The Enterprise segment might be cyclical eventually but the market is not saturated yet and we are still in the growth phase. In the short term, the Covid crisis will certainly be a dampener on growth. For most enterprise customers, this is capex but not a major item. Think of a hotel installing (or upgrading) WiFi on their premises.

The Service Provider segment is more mature but continues to see mid-single digit growth. For these customers, the equipment is a major capex but that capex is key to their business.

6. What is the longer term impact of 5G/LTE on the Service Provider segment?

Pera has been asked this question before. His reply: “I know LTE, like CPEs and LTE home consumer type service, has been around for a while. I don’t see it impacting. We really are a cable modem replacement or DSL modem replacement. People are going to always want, in my opinion, a hardline that’s unlimited capacity where they can download and run like Netflix continuously and not worry about overage charges. And big carriers also have expensive overheads – they gotta pay for the spectrum, they gotta pay for truck rolls. AirMax, from an economic perspective, is really barebones. You have sub-$100 IPs, you have CPEs that we are selling into the channel for, as low as, sub $40. You have entrepreneurs that are willing to roll up their sleeves and deploy all the infrastructure. We target a lot of rural areas where a lot of these big operators don’t want to make the investment. We are also diversified in different geographies of the world. But it’s quite possible they will start taking market share.”

7) What are some of the new areas the company is expanding in?

The opportunity in Video Cameras:

Ubiquiti is also making a bigger push into the networked security camera space, where a big opportunity has opened up in US and developed markets because of security concerns around Chinese companies like Hikvision and Dahua. Ubiquiti has a long and frustrated history in this segment; if you go back to Pera’s statements on this topic in past earnings calls, you can piece together the narrative.

Nov 2012 AirVision, our IP video surveillance platform has been re-architected and vastly upgraded with the announcement of our AirVision 2.0 NVR and management software. We expect strong growth in AirVision over the next year and going forward.

Aug 2013 I think AirVision, I think that’s going to have a big year next year.

Aug 2014 AirVision started out of the gate when we launched it 2 years ago with great traction. But we made some mistakes in the design architecture. Largely my mistakes, and we’ve corrected them. And we’re on AirVision 2, which is the second generation of the software, and it’s getting traction again. So my hopes is you’ll see a similar trajectory in our IP video security solution growth as you’ve seen with UniFi in the past couple of years.

Feb 2015 We started in 2012, and now we’re looking at three years later. And I think over the past three years, we’ve definitely made some mistakes, some rookie mistakes, especially on the hardware side and the software side. We definitely had issues, the hardware platform we chose, the network video recording, the NVR architecture, and the user experience. And I think what you’ll see this year is, our hardware, third-generation hardware is very, very good. Our NVR is greatly improved. And the final thing we’re missing is user experience…We have made a lot of improvements to the user experience to the software. So it’s not a significant contributor to UniFi today, but I expect it to be materially very significant in the next two to three years.

May 2015 Video is one of our initiatives I’m most excited about. We’ve been working on video for 6 or 7 years, and I think we’ve finally solved it. And the direction it’s going is, I think, pretty exciting. You’re going to see some new product announcements and some software leaps forward this year… I think this year, towards the end of the year, I think I’m expecting kind of an inflection point for that platform.

Aug 2016 I’ve been trying to do video since 2007, as embarrassing as that sounds, we’ve been at this since 2007. And what’s kind of disappointing about UniFi Video is we had the right idea. In 2010 or 2011 when we launched that platform…and we were there before Hikvision and a couple of the other dominant China players today. And we were there with a complete user experience from hardware to software to network video recording at a really disruptive price point. And everybody wanted that product. And if we executed, it’d probably be, I don’t know, hundreds of millions of dollars of revenue today. We just didn’t do it, and we missed the time window. But like we did with UniFi, we pretty much evolved the team, replaced the team over the past year, year and a half, two years, and we’ve made some fundamental changes to the controller. And you’re seeing now it’s more stable. The hardware is on generation three. It’s better. But we’re not done. I think by the end of this year, I think we’re going to make a pretty big step in video that’s going to boost its growth a lot more.

Aug 2017 Video is a huge opportunity for us, our solution isn’t that good today, it still sells hundreds of thousands of cameras a year. Once the underlying issues are fixed…I think you will see camera sales go from hundreds of thousands a year to millions a year… We also have more complimentary technologies to add to UniFi. Our vision is you go into a building one day and you will see UniFi running everything, everything from the automation to the lighting to the Wi-Fi piece to the door security systems to the video security systems and more.

Feb 2018 Another big catalyst in the UniFi world is video. We’ve overhauled the team and the R&D strategy about two years ago. And I think what you’ll see in the later half of this calendar year is UniFi Video turning the corner much like UniFi did in 2016, 2017. So we’re on our fourth generation of UniFi Video technology and we’re going to significantly reduce the pricing and significantly increase the performance and the user experience. And that’s all going to start in the next few months with the release of UniFi Video 4. [Hikvision’s issues in the American market started around mid-2018.]

May 2018 Video is picking up, we’re taking it into adjacent markets and we’re trying to create a complete collection of technology all consolidated within the one UniFi Controller platform… I think our next generation of video we finally got right.

Aug 2018 So, we are continuously making good cost reductions, but we also plan to continue to be aggressive on new product introductions. For example, video security is something I think we should have a much larger market share of and we are going to be very aggressive with UniFi video over the next couple of years.

To us, the salient points that emerge are:

1. Ubiquiti has been working on video surveillance for a long, long time; in fact Ubiquiti is already on its 4th generation of video surveillance products.

2. Pera keenly regrets the missed opportunity in surveillance systems; in his view, Ubiquiti fumbled the opportunity and gave it to Chinese players like Hikvision and Dahua.

3. Ubiquiti’s video offering is now integrated into a broader WiFi platform.

Not only is video surveillance a high-growth market, the size is large enough to have a significant impact on Ubiquiti’s numbers. We estimate Hikvision’s sales in the U.S. to be roughly $360 mil in 2018. Given Ubiquiti’s last-four-quarter revenues of $1.1 bil, Hikvision’s piece of the pie is significant for Ubiquiti.

While it’s true that Pera has had a history of overly optimistic expectations on the video surveillance front, (1) with Hikvision and other Chinese brands hobbled by security concerns, and (2) an improved product line that’s integrated into a larger WiFi system, we think that Ubiquiti’s competitive position is very strong this time. Pera knows that he fumbled this opportunity in the past, and we’re sure he’s going to make the most of this second bite at the apple.

Unifi Access: Door Access reimagined

Another example that shows how Ubiquiti’s Enterprise Wifi system can be a platform for additional functionality. After introducing video surveillance, Ubiquiti has just launched an access control system.

In Pt 1 (here), I introduced the American networking company Ubiquiti Inc and its founder Robert Pera. I discussed Ubiquiti’s products and their aggressive share buybacks.

In Pt 2 below, let’s explore why the company is so profitable. After all, they are funding these buybacks through the free-cash generated by the business.

In Part 3 (here), I put together our responses to the most common questions we get asked about our investment in Ubiquiti.

I first heard about Ubiquiti in Jan 2015 at an investor conference. Their financials seemed excellent (almost too good to be true) and the valuation was very cheap. It took me a couple of years to start understanding their business strategy and their prodigious cash generation.

Business model

Before we get into the competitive advantages of Ubiquiti, let’s understand how the company developed their unique and non-traditional business model.

“We believe that our products are highly differentiated due to our proprietary software protocol innovation, firmware expertise, and hardware design capabilities. This differentiation allows our portfolio to meet the demanding performance requirements of video, voice and data applications at prices that are a fraction of those offered by our competitors.

As a core part of our strategy, we have developed a differentiated business model for marketing and selling high volumes of carrier and enterprise-class communications platforms. Our business model is driven by a large, growing and highly engaged community of service providers, distributors, value added resellers, systems integrators and corporate IT professionals, which we refer to as the Ubiquiti Community.”

“Traditional company business models aren’t built to empower customers and pass on value to them. They are built to extract profitability from them. And information asymmetry gives them the perfect cover. But, with an increasingly connected world paving the way for more and more information transparency to the customer, all of this is about to change. No longer are “Insiders” able to control the flow of information. If a product is great, soon customers will tell other customers on the Web and rave reviews spread like wild fire. Similarly, if a product is bad or customers realize they are being ripped-off, relationships will provide little recourse to contain that information from being widely disseminated.

What does this mean moving forward? As an Engineer first who enjoys building great products, and a Businessman second who has no patience for politics and inefficiencies, I feel very fortunate to be at the early stages of my career in this point of time. Moving forward, I can say with certainty that the most successful tech companies of the future will be the ones who deliver the best products and technology value first and foremost which empower customers. This is very different than the traditional business model which leverages relationships to control information asymmetries and extract profit from customers.

Three companies that I believe are positioned well in an increasingly information transparent world are: Tesla (Electric Vehicles), Xiaomi (小米科技; Smartphones), and Ubiquiti Networks (Enterprise/Carrier Technology). What is important to note is that although these companies deliver technology value very efficiently, all take concentrated R&D approaches to produce leading edge performance products which in turn generate evangelism for their brands.”

The Old Model vs. The Future Model

To summarize Pera’s thoughts, Ubiquiti made good hardware at low prices. They differentiated their offerings through their software and support ecosystem. They also leveraged the internet to build direct relationships with their tech-savvy customers for sales and support and essentially outsourced most of sales and marketing – the cost savings were passed on to consumers.

Ubiquiti’s moat

Let’s delve into Ubiquiti’s business strategy in more detail to better understand the reasons for their profitability.

1. Culture:

Pera has built a unique engineer-friendly culture at Ubiquiti where small high-performance teams get a lot of responsibility and independence to experiment with ideas.

The company pays high salaries to their engineers as they understand that a great engineer can be ten-times better than a mediocre engineer. Outside of US, they’ve built research teams at locations like Lithuania and Taiwan where it is relatively cheaper to hire great engineers.

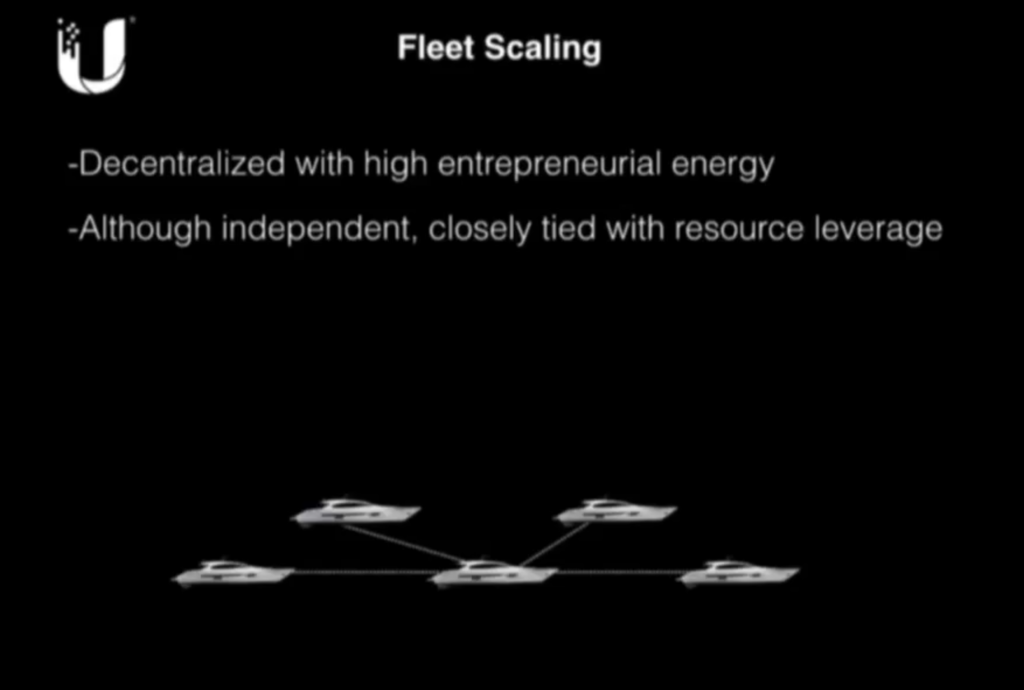

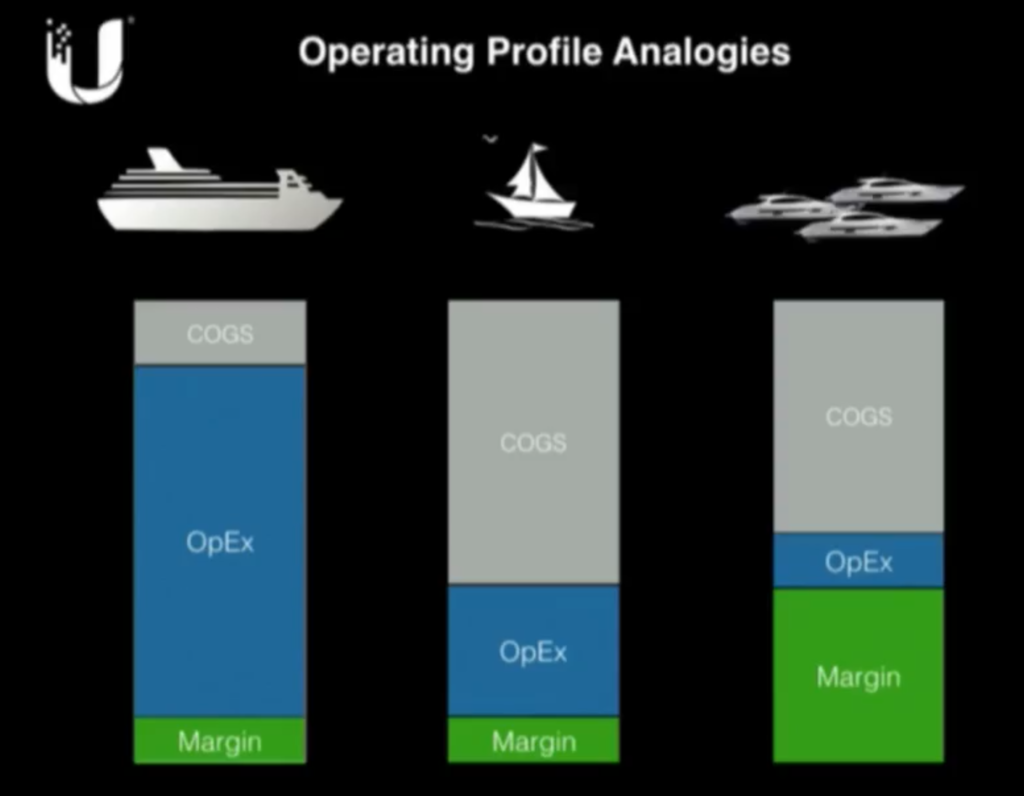

Ubiquiti’s organisational setup: “Fleet of aggressive ships”How Ubiquiti’s organisational structure manifests in the operating profile

The company also has a culture of transparency in communicating directly with their customers. Ubiquiti does not employ a large direct sales force, but instead drives brand awareness largely through the company’s user community where customers can interface directly with the company’s R&D, marketing, and support. These direct interactions with customers also provide a tight feedback loop for product and feature development.

2. Unique Sales Model:

Ubiquiti’s gross margins are actually not very high compared to the industry – see table below:

Ubiquiti’s operating profile versus the sector

Despite average gross margins, they are still so profitable because their sales model is completely different (from competitors). From their 10K: “We do not employ a traditional direct sales force, but instead drive brand awareness through online reviews and publications, our website, its distributors and the company’s user community where customers can interface directly with R&D, marketing, and support”:

Traditional competitors like Cisco find it very difficult to compete with this model as they have a large existing sales force and any transition towards a direct-selling model is very painful as it would involve lower margins and cannibalisation of existing business.

3. Customer lock-in and high switching costs that come from building sustainable platforms/ecosystems:

From a good writeup on Ubiquiti’s ecosystem by Michael Huber (in 2017): “In the first instance, the ecosystem’s power is derived from communities. While investors unfamiliar with networking can debate the number of logins on the communities and whether they are boosted by the presence of bots, these arguments entirely miss the point. If you are deploying a network and you have a problem with Ubiquiti equipment, or even just a question that may not be directly related to Ubiquiti, you can log in to the Ubiquiti community, search your problem, and find an answer almost 100% of the time as all past discussion streams are cataloged and searchable. This is a major shift in power away from the pay for support model, where the cost is not just the support contract but the time wasted getting to the right person to get the answer. As a result, the Ubiquiti ecosystem enables non-experts to deploy and troubleshoot basic networks. Not only does the equipment cost half or less than competitor products, there is no service contract to be purchased, and you can deploy the equipment with the IT staff you already have without having to hire or certify new IT staff people.

Similarly, in the WISP space, Ubiquiti’s technology can be deployed by the many small operators without having to find expensive, highly certified technicians who, incidentally, don’t tend to live in the areas where WISPs operate. We attended WISPAPALOOZA last week in Las Vegas, and WISPS are typically run by scrappy entrepreneurs. Ubiquiti gives them a way to learn to do things themselves, which saves them time and money, and it’s a core part of their success. The community, and the many years of troubleshooting history it contains, is an enormous asset to Ubiquiti’s carrier customers.

The communities, however, are actually the old news. The more recent news are the software platforms and apps that Ubiquiti has rolled out in recent years: Unifi for the enterprise; Video for their video products; Umobile for the Airmax products. There are a two things to note about these platforms:

1) they are cloud based software platforms that are free and, once set up, enable Ubiquiti’s products to be provisioned, updated, rebooted and monitored by anyone with an iPhone.”

2) they provide tremendous visibility into the network quality, usage patterns and facilitate network troubleshooting.

Are these products unique to Ubiquiti? No, but they are excellent products and come free with Ubiquiti’s already inexpensive products. Furthermore, once you have them deployed, they make it extremely easy for anyone with permission to add additional Ubiquiti products to the platform, which drives future sales.“

4. Integrated systems and encryption make it difficult for competitors to clone their products

One of the obvious questions is what stops their Asian OEMs (or other competitors) from producing similar gear themselves and selling it at a lower price?

The answer is that hardware is only one part of the overall system. Their integrated software ecosystem is not easy to replicate. Let’s go back to the company’s early days to see what happened.

“In 2005, Ubiquiti would launch its first product called “SuperRange” – essentially a super-charged Wi-Fi module for long-distance outdoor wireless applications… The appeal of our “SuperRange” module was that it performed better over long-distances compared with the standard commodity Wi-Fi modules being sold in volume…

However, there were 2 disastrous variables working in the background that would inevitably be fatal to my initial business strategy:

Our $35 manufacturing cost was representative of our economies of scale in 1,000’s of quantities. In contrast, the popular commodity modules had a $20 resale price were coming from Asia in 1,000,000’s of quantities. Interestingly, there was no significant intrinsic design or manufacturing cost premium in our enhanced design compared to the commonly sold commodity module. We were just completely outmatched with our competitors from a manufacturing volume/cost leverage standpoint.

Our improvements were simple HW design additions that could easily be copied

You can imagine what happened next. The commodity Wi-Fi module manufacturers soon noticed our growing business and gross margins and said “Hey, this is a great idea; we can manufacture a premium module design and take over their market” Within months, they copied our HW design and clones started appearing in our sales channels at below our manufacturing costs.

Overnight, growth slowed, customers turned on us saying we had no business selling such over-priced hardware, and I found myself in an impossible position to compete; I was contemplating shutting the doors and moving on with my life.

…

When Ubiquiti was faced with instant commoditization from lower-cost Asia competitor clones shortly after our initial radio module release, I quickly was forced to change development directions. I knew we could never compete with Asia competitors in a hardware only module business; if we were to survive, we had to go upstream and compete with our system customers. This would mean pulling together development resources that could deliver a complete solution to market that included investment into system hardware design, mechanical design, antenna design, and firmware development.”

Encryption: In Ubiquiti’s early days, they also had issues when one of their suppliers started to produce duplicate products and sell them as fake Ubiquiti products. To counter this, they now also build in encryption keys in all their devices so fake products don’t work with the rest of the Ubiquiti ecosystem.

The company’s hard learnt lessons from the early days made them laser focused on developing their proprietary software ecosystems as well as encryption that made copycat products incompatible with Ubiquiti’s ecosystem.

A company’s moat typically manifests itself in the form of profitable growth and Ubiquiti has been exceptional both in developing new products to grow the business as well as maintaining high profitability.

Revenue Growth by Segments

Along with good revenue growth, their gross margins have gradually improved from 42.2% in FY13 to 47.3% in FY20 – this is partially due to their operational improvements and partially as the Enterprise segment has slightly higher gross margins versus the Service Provider segment.

Financials and Valuation

Over the last seven years since FY13 (which was the first year excluding the IPO year) to FY20, Ubiquiti has grown:

topline from $321mn to $1.3bn (CAGR of 21.9%) – as they expanded into new areas and adjacent product lines

operating profit from $93mn to $478mn (CAGR of 26.4%)

net profit from $81mn to $380mn (CAGR of 24.8%)

(diluted) EPS from $0.89 to $5.80 (CAGR of 30.7%) – because of aggressive and well-timed share buybacks

free cash flow from $127mn to $430mn (CAGR of 28.7%)

It’s worth noting that we don’t need to make a lot of adjustments to Ubiquiti’s financials. They rarely hand out stock options so their accounting earnings and cash flows track closely over time. They are also very capital efficient: in FY20, their total capex was just $31 million.

In FY20 (latest year ending June), Ubiquiti generated ~$430 million in free cash flow. At their recent share price of US$160 per share, their enterprise value is around $10.8bn (mkt cap $10.3bn, debt $680mn, cash $144mn). So the company is trading at 25 times free cash flow or ~4% free cash flow yield. We feel this yield is more “real” than in other companies because management has been very disciplined about capital management and very aggressive about returning capital to shareholders.

For us, valuation is about getting a margin of safety to our purchase price. In the case of Ubiquiti, even without building in any growth, current valuation is reasonable if this level of cash flows can sustain. And the company’s stock buyback provides a very strong support less than 15% below current levels. They were recently buying back stock at $138 and, in another year’s time, will probably raise this price above $160. [Please note that the original article was written in September and references the share price at the time].

In our opinion, the key driver to watch is long term revenue growth in their Enterprise Segment which has, at least in the short term, taken a hit. We think this is a temporary hit due to Covid.

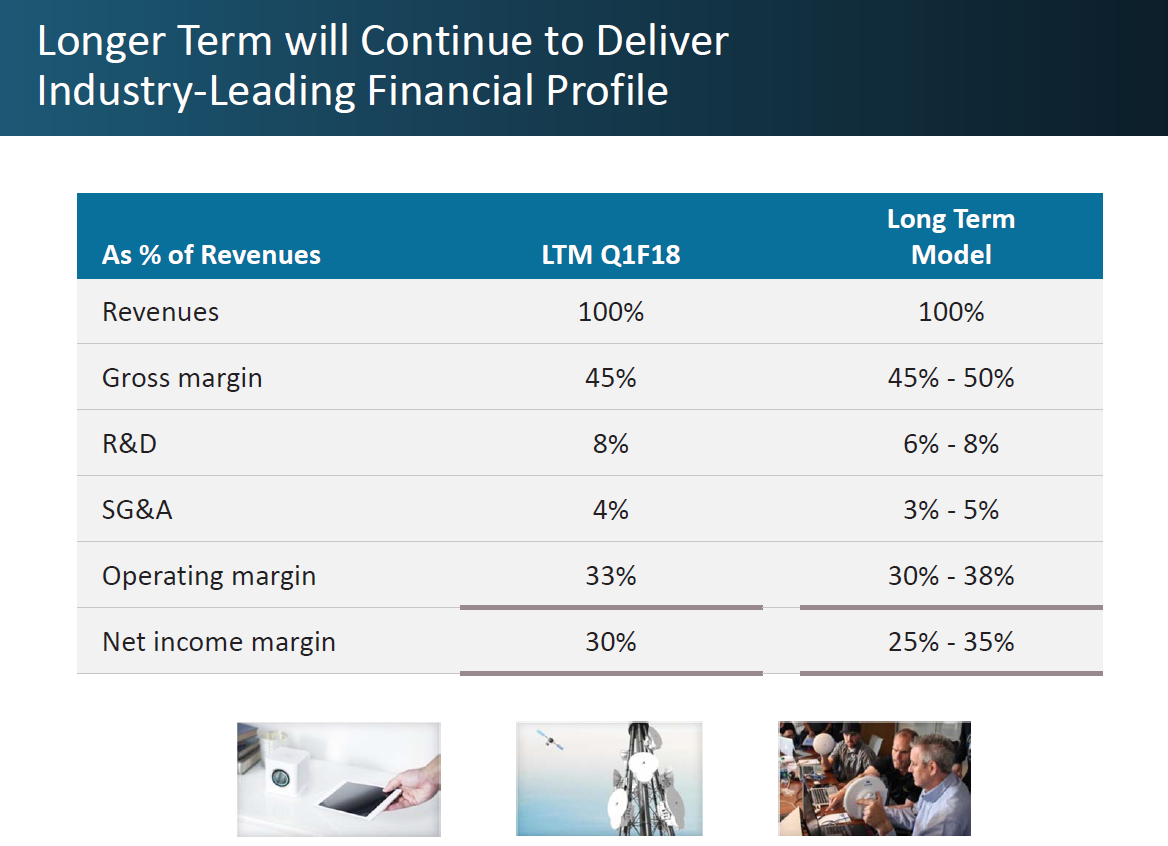

In their last investor presentation in Nov 2017, the company had provided their own long term expectation of how their financial profile will look like. So far, it has been a good roadmap for building a financial model.

Ubiquiti’s Main Competitors

Backhaul

Cambium Networks, Ceragon Networks, DragonWave, MikroTîkls, Airspan, SAF Tehnika and Trango

CPE (routers, switches, gateways etc)

Cambium Networks, MikroTîkls, Ruckus Wireless (Arris) and TP-LINK Technologies

Disclaimer: Our firm owns shares of Ubiquiti. This is not a recommendation to buy, sell, or hold the stock. We may change our mind on the company at any time without informing you (or updating the blog). You shouldn’t be taking investment advice from a stranger on the internet anyway.

Ubiquiti is one of the most interesting companies I track that very few people have heard of. Our firm has been a shareholder of the company since early 2017. This blog post is the first of a series that I plan to write discussing the company and its media-shy founder in detail.

Robert Pera’s header on Twitter

Ubiquiti was started in 2005 by Robert Pera, a former Apple engineer, in his studio apartment. The company has been profitable every year since its inception (all except FY10 when they were facing copycat products). As a result, it never needed to raise venture funding which is partly why Pera still maintains a high ownership stake. Ubiquiti currently has a market capitalization of roughly US$12 billion. Pera owns 88% of the company which means his stake in the company is worth over $10 billion. He takes no salary (never took a salary and never gave himself stock compensation) and continues to be the driving force behind the company. It is worth noting that he is only 42 years old.

Tracking the company is not easy anymore as they have stopped doing investor calls or providing forward financial guidance since 2018. As the free float of the company has gotten smaller and smaller, Pera probably just felt that it wasn’t worth his time. It’s even possible that, at some point, he buys out the remaining shareholders and takes the company private. We can still get bits of insight from their quarterly financial releases but we have to rely on historical presentations to understand the company strategy. I hope this writeup provides some context on why we think it’s such an interesting company.

“Ubiquiti Networks was bootstrapped with no operational funding from inception up to the IPO. For a software company, this path is challenging enough. But, Ubiquiti makes hardware. And with making hardware comes the additional financial burden of funding larger and larger manufacturing expenses as the business grows.

When I left my job at Apple in 2005 to dedicate myself to Ubiquiti, my only thought was “if this doesn’t work out, I am screwed.” It was March of 2005 and my $600/month studio apartment lease down the street from Apple HQ was coming up for renewal. Instead of committing to another year, I moved my futon and my HW lab into an economical $650/month office surrounded by bail bonds shops across the street from the San Jose Courthouse where I would make my home for the next several months. Although there was sufficient capital from upfront customer down payments to fund the first manufacturing builds, I was locked in survival mode and entirely focused on how I was going to setup manufacturing, make the shipment lead-times, support initial customers, come up with new product designs, and build the Ubiquiti brand.

In 2005, Ubiquiti would launch its first product called “SuperRange” – essentially a super-charged Wi-Fi module for long-distance outdoor wireless applications.

Because the product had incredible demand from a niche market of independent operators and distributors that served them, we were able to secure customer payment upfront to fund manufacturing and instantly became a profitable business with cash flow.“

What does the company do?

Ubiquiti makes products and solutions in two main categories: high performance networking technology for 1) service providers and, 2) enterprises. They also have a small consumer business. They manufacture their products through OEMs (Original Equipment Manufacturers) in China, Taiwan and Vietnam.

Service Provider segment (roughly 1/3rd of overall revenues) is mainly network infrastructure for fixed wireless broadband, wireless backhaul systems and routing, and the related software for WISPs (Wireless ISPs) to easily control, track and bill their customers. Wireless broadband uses microwave transmission to connect remote areas to the internet where laying fiber would not be economical due to low user density. The customers are mainly WISPs who tend to be small entrepreneurs looking to deploy internet in their locality. This is now a mature and stable segment growing in mid-single digits.

Enterprise WiFi segment (roughly 2/3rds of overall revenues) is mainly equipment used to deploy a wireless LAN (“WLAN”) infrastructure over a large area, such as a hotel, university campus, or large office complex. This segment also includes video surveillance products, switching and routing solutions, security gateways, and other complimentary WLAN products along with Ubiquiti’s Unifi software platform, which enables users to control and monitor their network from one simple, easy to use software interface. The Enterprise segment has been driving the overall growth in the last few years though it slowed down in the recent quarter due to the impact from the ongoing Covid-19 crisis.

In addition, Ubiquiti has started a line of consumer-oriented WiFi mesh equipment for the home but this remains small – mainly since the company doesn’t do a good job of selling to retail consumers. But this segment doesn’t move the needle. The company now combines the revenues it gets from this segment into the Enterprise segment.

Ubiquiti’s business segments (Source: Ubiquiti Investor Presentation)

Their sales is well-diversified globally (see table below) though still primarily in developed markets:

Revenue split by geography – from company filings

Following the cash: share repurchase history and dividends

Ubiquiti went public in Oct 2011 raising US$106 million (7.04 million shares at their IPO price of $15). Even in the IPO, almost 2/3rds of the money was secondary placement, which was mainly their private equity investors cashing out, so the company essentially raised ~$37 million in primary issuance which was used to pay off a convertible-debt tranche. Meanwhile, since the IPO, the company has returned $2 billion in stock buybacks and $180 million in cash dividends to investors.

If Ubiquiti is a fraud (as some short-sellers alleged), where did this $2.2 billion come from?

And management could easily pay themselves a hefty salary or pay out a high dividend (which would largely go to Pera as he owns most of the shares)? Instead, they mainly bought back shares with the free cash flow!

Ubiquiti the Cannibal

Charlie Munger, vice-chairman of Berkshire Hathaway, says “pay attention to the cannibals”. He means we should closely look at cash-rich undervalued businesses that are buying back huge amounts of their stock as these businesses can generate a lot of value for their shareholders.

Well, Ubiquiti generates a ton of free cash and management has an excellent track record of aggressively buying back shares when they are priced cheap (as can be seen in the table below):

Ubiquiti’s history of share repurchases and cash dividends

Since their IPO, Ubiquiti’s free float has gone down from 36.2mn shares to 7.5mn shares currently – a reduction of almost 80%!

Pera has mentioned being a fan of Henry Singleton of Teledyne who bought back 90% of the outstanding stock of Teledyne when it was trading cheap. He is clearly following in Singleton’s footsteps.

The disappearance of Ubiquiti Inc

Currently, Ubiquiti has an outstanding share repurchase program worth ~$538 million. Their free-float is just ~7.5 mn shares. At the recent share price (~ $183.5), the free-float is worth $1.2 bn so the buyback is for almost ~40% of the outstanding free-float. The company was recently buying back shares at $138. This is an excellent asymmetric risk-reward situation.

In Part 2 (here), I discuss Ubiquiti’s business model and how they are able to maintain their high profitability.

In Part 3 (here), I put together our responses to the most common questions we get asked about our investment in Ubiquiti.

Disclaimer: Our firm owns shares of Ubiquiti. This is not a recommendation to buy, sell, or hold the stock. We may change our mind on the company at any time without informing you (or updating the blog). You shouldn’t be taking investment advice from a stranger on the internet anyway.

Netflix is the poster child of a company that has benefited from Covid-19 related lock downs as people are forced to stay at home. It is not surprising that their stock price is up roughly 50% this year alone. However, it is still not too late. In fact, we think that the Covid-19 crisis has substantially reduced the risks facing Netflix and improved the risk-reward equation of owning the stock now.

Our firm had a small sized investment in Netflix since late 2019. We had kept it small because, at that time, there were considerable risks facing the business.

First, several competing streaming services were about to launch, including Disney+, Apple TV+, ABC’s Peacock, HBO Max, and Quibi.

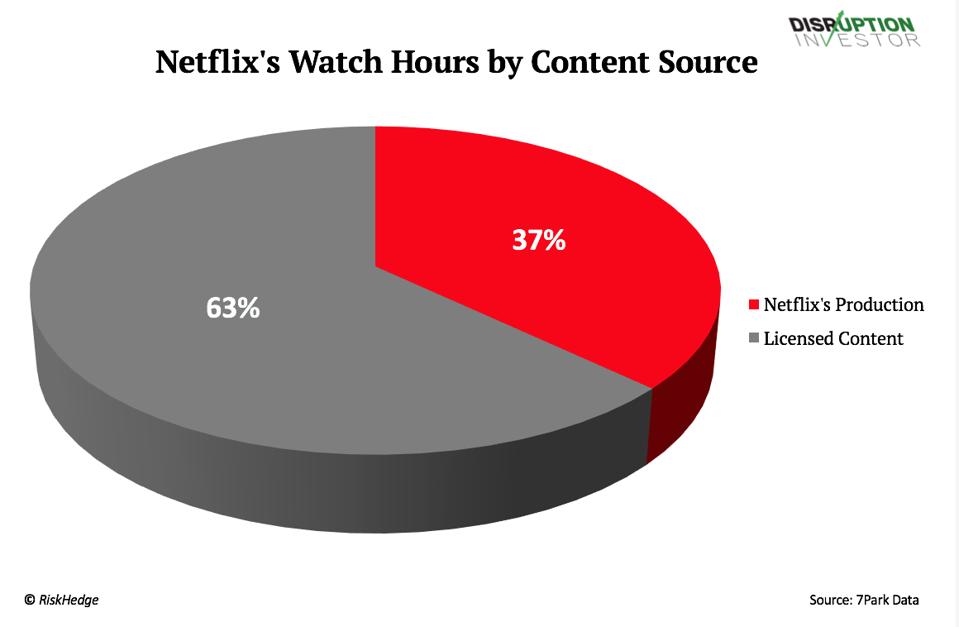

Second, Netflix was about to lose a big chunk of their licensed content which accounted for more than half of their viewing hours (primarily Disney-owned content but also popular shows like Friends, to HBO Max, and The Office, to Peacock).

Netflix’s watch hours by content source RISKHEDGE 2019

In Nov 2019, the day before Disney+ was launching, Stephen McBride wrote in a column in Forbes titled ‘In 24 hours, Netflix could lose almost 25% of its subscribers‘: “the future of streaming belongs to content creators. To its credit, Netflix has changed the way we watch TV. But after 20 years, it’s still a company that “rents movies’… but now it’s doing it over the internet. It’s still just a middleman. Now that Hollywood giants have woken up, it’s only a matter of time before they catch up to Netflix. For Netflix, the battle is lost. While Hollywood spent decades and decades piling up the archives of blockbusters that span multiple generations, Netflix has just started the process.“

Third, in addition to the traditional Hollywood brigade, Apple and Amazon were looking to create original content as well, threatening to bid up costs.

Fourth, it was unclear if Netflix’s aggressive spending on original shows would pay off given the competition as well as worries about their long-term pricing power.

All these risks made it hard to value the company as the range of possibilities (both around increasing subscribers and around increasing pricing) was very wide.

What changed this year?

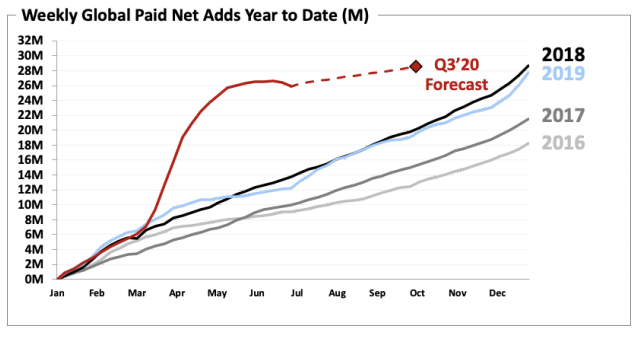

Netflix subscriber growth pattern by year

Netflix added ~16 million new subscribers in 1Q followed by ~10 million new subscribers in 2Q. To put that in context, they added 28 million new subscribers in all of 2019. This growth spurt due to the Coronavirus crisis brought their total subscriber base to 193 million. Commenting on their subscriber growth, Ben Thompson, who is one of the best technology analysts covering the company, wrote “I do think the financial impacts of this pull-forward are being under-appreciated: 8 million subscribers signing up 6 months sooner than they would have otherwise, to pull two numbers out of thin air, is worth an additional $84 million per month in revenue, and given that that is for a subscription, it is revenue that is additive to however much Netflix would have earned from them in the future. Similarly, the money that Netflix is saving on content production that isn’t happening is likely to push back other production in years to come; this quarter’s unexpected positive cash flow doesn’t necessarily mean that Netflix has to pay it back in the future.“

In other words, the positive effects of accelerated subscriber growth are not temporary. As lockdowns end and people start venturing out of their homes, average viewing hours per customer will come down…but that is not the same as saying that ARPU (average revenue per user) or total revenue will come down. Netflix’s topline will continue to benefit from the increased subscriber base. There might be some increase in churn but fears of en masse subscription cancellations are overblown.

Further, this is a business where there are incredible returns at scale. In Jan 2019, Barry Diller, chairman of IAC (which owns multiple media and internet brands across 100 countries), said, “Once [Netflix] has built up to 200 million or so subscribers, it’s very hard for anybody to come close. Eventually, the dollars will rationalize, and I think [Netflix’s] cash flow will be huge”. With the recent bump in subscribers, Netflix has created an incredible lead.

Meanwhile, most of the competitors (Disney+, Apple TV+, HBO Max, Peacock, and Quibi) have already launched their streaming services. Except for Disney+, most have been underwhelming if not outright failures.

The crisis has blunted the competitiveness of Disney+ also. Although it provided an immediate subscriber boost shortly after launch, it also reduced Disney’s financial resources and management attention as the company’s movie and theme parks divisions remain crippled.

The crisis has also slowed down content creation for everyone else, as the production of many shows get halted by the virus, while Netflix (due to its aggressive investment in content last year and its tendency to produce entire seasons of shows upfront) is less affected. Netflix elaborated on this point in their Q1 shareholder letter: “Well, the one thing that’s maybe not widely understood is we work really far out relative to the industry because we launch our shows all episodes at once. And we’re working far out all over the world. So our 2020 slate of series and films are largely shot and are in postproduction remotely in locations all over the world, and we’re actually pretty deep into our 2021 slate. So we aren’t anticipating moving things around.“

The upshot is that Netflix represents a safer value proposition now than it did a couple of years ago. Investing is about gauging risk-reward, and we feel the Covid-19 crisis has substantially reduced the risk to Netflix’s investment thesis.

The long-term investment case

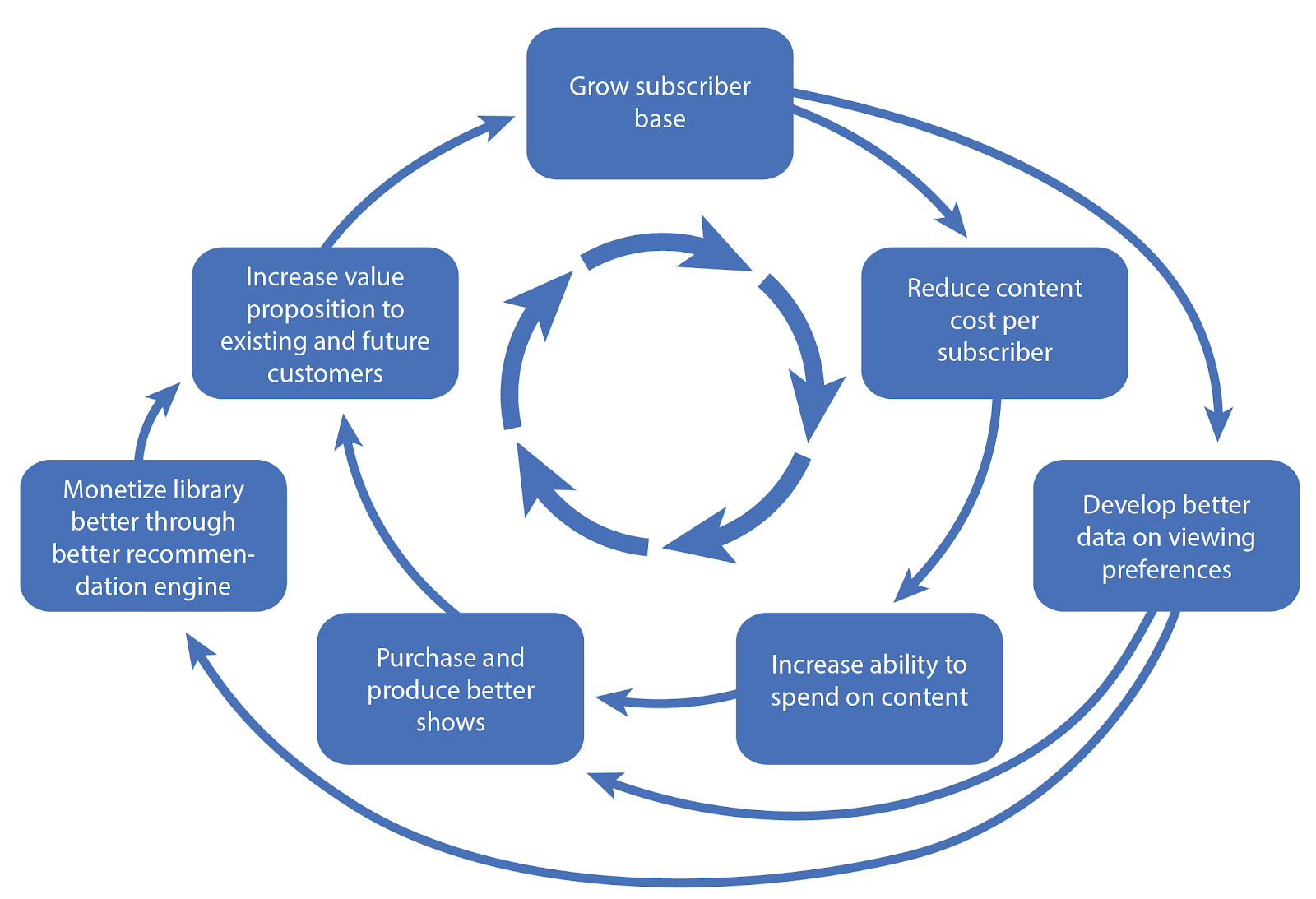

Given Netflix’s business model, where the marginal cost of serving a new subscriber is essentially zero, it has been clear for a few years already that Netflix would dominate their segment if they had 1) the most subscribers, 2) a good enough content library, and 3) effective recommendation algorithms to surface relevant content for each subscriber.

The Netflix Flywheel

Now that Netflix has the largest subscriber base by far, their flywheel is spinning at full speed. In a recent interview, Matthew Ball, former head of strategy at Amazon Studios, said: “If Netflix can launch worse content to greater success than you can, and because of its greater scale it can economically do that, that’s a huge advantage.”

Netflix already spends around $17 billion on content annually – more than anyone except for Disney – and we expect this to flatten out at around $30 billion annually in a decade. Soon, many of their sub-scale competitors will realize that they can make more money selling/licensing their content to Netflix (which can monetize that content much more effectively) versus trying to build up their own streaming businesses.

Over time, Netflix’s value proposition to existing and future customers will continue to go up as they add content at a furious pace. It is also clear that as the value proposition of their content library improves, Netflix will increase prices.

At scale, the combination of higher subscription charges combined with flattening content costs will generate prodigious cash flows.

Thoughts on valuation

It is not an easy task to value Netflix precisely when they are still focused on rapidly growing subscribers and cementing their lead as the dominant global media streaming company. However, it is easy to see that this is an incredibly profitable business at scale.

The recent quarterly results provided a glimpse of just how profitable Netflix will be once they have saturated the market. In the recent quarterly investor letter, management said, “We’re often asked by investors what our FCF profile would be at “steady state” or when our cash content spending matches our content amortization. The pandemic and the resulting pause in productions provides one early snapshot of what that may look like. In Q2’20, our cash spending on content was $2.6 billion, equivalent to our content amortization of $2.6 billion, or a 1x cash content-to-content amortization ratio. This resulted in a FCF margin of +15% in Q2. Of course, our plan is to continue to grow our content spend (as we don’t believe we are anywhere near maturity), but the above analysis may prove illustrative.”

Our expectation is that once Netflix has saturated their potential subscriber base, their expenses will also start to rationalize, and the full pricing power will come to bear. Based on our projections, in five years, Netflix should reach 350-400 million subscribers and ARPU should go up to ~US$15 (maybe even $20 in an optimistic scenario). If our projections prove accurate, we think Netflix can easily trade at a market cap of US$400-600 billion in five years versus their current market cap of US$210 billion (which is equivalent to ~US$480 per share). This should provide a mid-to-high teens returns CAGR from current levels.

We also think that a dominant consumer facing application like Netflix with 350-400 million engaged subscribers will provide multiple opportunities to make money outside of the core subscription model. These could deliver further upside to our estimates depending on how management decides to pursue these alternate paths.

Given the attractive risk-reward, we recently increased the size of our investment in Netflix.

P.S. This post is excerpted from our firm’s recent investor letter which my partner GC and I wrote together.

Disclaimer: Our firm owns shares of Netflix. This is not a recommendation to buy, sell, or hold the stock. We may change our mind on the company at any time without informing you (or updating the blog). You shouldn’t be taking investment advice from a stranger on the internet anyway.

I moved to Hong Kong in 2007 after completing my MBA to join Merrill Lynch in their exotic derivatives team. It was a dream job and I was super excited. Life was good – things were going according to plan. So imagine my shock two years later when, in the wake of the financial crisis, I found myself redundant and out of a job.

It was perhaps at that moment that I began to understand what it means to get hit by the tail-end consequences of a black swan event.

Luckily, a few months later, I managed to find another job. I joined Blue Pool Capital, an Asian hedge fund, as a junior analyst. Blue Pool later converted into a family office for a few of Alibaba’s founders. I spent over six years at Blue Pool researching companies and investment opportunities in Asia. It was a small team and they gave me considerable freedom to experiment with all the crazy ideas I had. I met some incredible people and learnt a lot about markets and investing during my time there.

When I look back and try to connect the dots, it was perhaps the events of 2009 that shaped my desire to create an anti-fragile life. So it was partly towards that goal that I finally left Blue Pool, partnered with a friend and colleague, and started Asymmetrics Capital in 2016.

I am often asked why we chose this name for our investment firm. In truth, I had been fascinated with Nassim Taleb’s ideas of asymmetry and anti-fragility for many years and wanted these ideas to be the bedrock of our new firm.

Our guiding principle, ‘Asymmetrics’, refers to our portfolio of asymmetric bets. Each of our investments have asymmetric return potential versus the risk taken. There is reasonable diversification across our investments so our overall portfolio is not vulnerable to a single factor. On top of this, we use leverage cautiously and in small doses.

Over economic cycles, we hope our carefully chosen well-diversified collection of asymmetric bets generates satisfactory returns while never taking a ruinous level of risk. We manage the fund with an eye on the resilience of the entire portfolio, trying to avoid concentration risk in any one geography, industry, or strategy.

How did we design the firm differently? Appropriate incentives and skin-in-the-game

After being a part of the hedge fund industry for over six years (longer for my partner), we were disappointed with the way most funds were set-up.

The standard hedge fund charges 2% of assets every year plus another 20% of the profits, commonly known as the 2-and-20 fee structure. We felt that this fee structure was not conducive to long-term success, not for fund performance, and especially not for investors’ returns after fees.

We thought of multiple ways to address the shortcomings of the standard hedge fund set-up. First, we wanted a structure that allowed us to implement a long-term strategy: to invest flexibly and patiently, shielded from the pressures and biases that the standard playbook creates. Second, we wanted our risks and incentives to be fully aligned with that of investors. Third, we wanted the fund’s fee structure to be fairer to investors – fund managers should not be richly rewarded for just getting lucky.

To fix these issues, we designed our fund with the following structural features which align our incentives with our shareholders:

1. Significant personal investment: Both managers have the bulk of our families’ net worth invested in the fund. Our interests are substantially aligned with our investors: we don’t take undue risks because we bear the downside as much as, if not more than, them.

2. Low cost operations: We were very focused on keeping our firm’s operating costs low which ensured that we broke-even at an early stage. This allowed us the luxury to be selective about raising capital from like-minded long-term investors. We have seen several funds perform poorly because they felt excessive pressure to shoot for short-term gains so they could raise capital on the back of that track record.

3. Limits on fund size: Rapid increases in fund size can create a significant drag on performance. Often fund managers say that they will close their fund to new investors after hitting a certain size but forget these commitments when faced with the opportunity to take in more money. Our fund’s foundation documents have an unusual provision contractually slowing down fund inflows after the fund hits a certain size.

4. Fair fee structure: We only earn a performance fee if we exceed a hurdle rate that compounds each year. This structure offers a fairer deal to our investors: we only earn our performance fee if we earn a return over that hurdle. In conjunction with our low management fee, our fee structure results in substantially better economics for investors over time versus a typical 2-and-20 hedge fund. In most situations, we estimate investors in our fund pay less than half the fees as compared to a 2-and-20 hedge fund.

The result of our structure is a fund that allows us to adhere to our long-term investing style and therefore positions us to generate good long-term returns. We invest patiently and don’t generate activity for the sake of activity. Cash is our default option if we can’t find suitable investments, but our required return hurdle discourages sitting on too much cash – this structure strikes a good balance between conservative and opportunistic. At the same time, because of our high personal exposure, we manage the overall portfolio risk very carefully.

We don’t think of risk as volatility or some abstract academic construct. Most of our families’ net worth is invested in the fund along with our investors. For us, the real risk is permanently losing a significant portion of these savings. Whenever we wrestle with greed, we are always keenly aware of what we are risking on the line.

The asymmetric outcome

After four years of running the fund, we are more confident that our set-up is indeed conducive to good performance. We have outperformed relevant indices while taking significantly less risk.

To sum up, our investment goal was to construct a portfolio which generates satisfactory long-term returns with minimal risk of catastrophic loss of capital, no matter which version of the world unfolds…and it is important to remember that though only one version eventually takes place, we could have easily landed in many different parallel universes.

Our firm embodies this attempt to cut off the left-tail of the risk-reward distribution and to position for favourable outcomes, hence the name ‘Asymmetrics’.

P.S. Though he hates limelight and is intensely private, I still wanted to give a shoutout to my co-founder GC. Asymmetrics is our joint effort and we have built the firm and developed these foundational principles together.

Great quote by Nassim Taleb and one that particularly resonates with me at this time: “How much you truly “believe’ in something can only be manifested through what you are willing to risk for it.”

Summary of course: Learning How to Learn: Powerful mental tools to help you master tough subjects – by Dr. Terrence Sejnowski, Dr. Barbara Oakley

Focused vs diffused mode: Our minds can only be in one of these two modes at a given time. Focused mode is when we concentrate intensely on a particular topic or concept. Diffused mode is when we are in a more relaxed state while sleeping, jogging, showering, etc. To learn faster, we should switch back-and-forth between the two modes so the neural mortar gets a chance to dry. A good analogy is with bodybuilding: focused state is a short exercise session followed by diffused state which is the resting phase. Both phases are important.

Chunking: Our working memory has only four slots versus the long term memory which can store vast amounts of information. Chunking refers to pieces of information tied together into a conceptual chunk. These are compact packages of concepts that can easily be accessed by our brains. These can also be thought of as a network of neurons that are used to firing together which makes it easy to access the entire chunk. Once chunked, a concept takes up only one slot in the working memory. We can form mini-chunks with deliberate practice. Small chunks can become larger with practice. Abstract concepts require more practice to strengthen the neural patterns. Learning happens at the edges – when there is slight discomfort or difficulty in grasping the concept. Solving a problem that has been solved before is not a waste of time – only by doing it do we create the unique neural patterns in our mind which helps master the concept. Chunking can also be thought of as bottom-up learning. This should be coupled with top-down learning which involves fitting the chunk into a larger conceptual framework. A good collection of mental “chunks” can make it easier to learn new things. This is the concept of “transfer” i.e. a chunk in one area can make it easier to learn a chunk in another area.

Procrastination: Pomodoro technique is a good way to avoid procrastination. First, set a time for 25 mins. Make sure there are no distractions in that time and concentrate on the task at hand. Afterwards, give yourself a small reward/treat to associate something positive for completing the session.

Procrastination and Memory: Habits have four parts: Cue (location, time, how you feel, reaction e.g. to email), Routine, Reward, and Belief. Procrastination is a habit. To prevent procrastination, focus on the process and not on the product. For instance, decide to spend 25 mins on homework rather than deciding to complete the homework. Some more techniques to reduce procrastination: keeping a planner journal, making lists of items for next day, doing the most disagreeable tasks first, rewarding yourself on accomplishing items but delaying rewards till the tasks are done, keeping a finish time for each day’s tasks, committing yourself to certain routines and tasks each day.

Ways to prevent illusions of competence: a) Recall. b) Mini-testing. c) Explain the concept to yourself aka Feynman technique. d) Highlighting too much can be ineffective – instead, write notes in the margin that help synthesize the material. e) Recall the material outside the normal place of learning.

Other key techniques for effective learning: a) Spaced repetition, b) Physical exercise also improves learning. c) In a boring lecture, ask a question – that will keep you more engaged. d) Being in a rich environment improves learning. e) Law of serendipity: don’t worry about remembering everything. Focus on one small concept. Later concepts will get absorbed more easily. Luck favors the one who tries. f) Overlearning: don’t overlearn during a single session. g) Einstellung (German for installation): This is when existing ideas / knowledge prevent better ideas from coming in. Charlie Munger uses the analogy of sperms and egg. As soon as a single sperm enters the egg, the egg shuts down preventing other sperms from entering. h) Interleaving i.e. mixing up the learning: This involves jumping back and forth between problems that require different chunks which helps to learn when to use a concept not just how. i) Switch between words and images. j) Zoom in and out to see the problem at different levels. j) Writing something down helps cement it in the brain. k) Reading a difficult piece: read other reference material to understand the surrounding context. Sometimes a writer can have good ideas even if they can’t express it well. k) Repitition in memorable ways can help cement a concept into memory. This creates more neural hooks on which a concept hangs.

Personality traits positively correlated with creativity and great achievement: a) openness to new experiences. b) Disagreeableness or non-conformism e.g. Steve Jobs

Jordan Ellenberg’s “How Not to Be Wrong: The Power of Mathematical Thinking” just went up on my summer reading list after reading this excerpt from a review of the book:

“During World War II, the U.S. military was trying to optimize the armor plating on its airplanes. Officials noticed that the bullet holes in planes returning from combat in Europe followed certain patterns: There were more per square foot in the fuselage than in the engine section. They figured that they therefore needed to add more protection to the fuselage, but wanted help in determining how much more — to balance the extra protection against the loss of fuel efficiency and maneuverability.

The military took this problem to Abraham Wald of the Statistical Research Group. Wald, who spent most of his career as a statistics professor at Columbia University, came back with a surprising answer: Add no plating to the fuselage. Instead, add it to the engine area.

Wald’s reason was that unless the enemy was for some odd reason successfully targeting the fuselages, the bullet holes on the returning planes showed where the planes could withstand attack and still survive. The paucity of bullet holes on the engine casings of the returning planes suggested that hits to that area tended to bring down the plane. Returning planes, in other words, were a biased sample of the planes that were attacked. The lesson: Think about where the bullet holes aren’t.“

Charlie Munger: “Experience tends to confirm a long-held notion that being prepared, on a few occasions in a lifetime, to act promptly in scale, in doing some simple and logical thing, will often dramatically improve the financial results of that lifetime. A few major opportunities, clearly recognizable as such, will usually come to one who continuously searches and waits, with a curious mind that loves diagnosis involving multiple variables. And then all that is required is a willingness to bet heavily when the odds are extremely favorable, using resources available as a result of prudence and patience in the past“